I stumbled happily upon The Long Tail yesterday, a new economic model for the digital age by Chris Anderson, the editor-in-chief of Wired. It came up in the context of a new division created by Anheuser-Busch within their company to explore new products, but more about that later. His economic model originated in an article he wrote in the October 2004 issue of Wired Magazine, which is where the term “the long tail” was first coined. Anderson has expanded it into a book of the same name which is coming out next month and he has a blog about it, too. The Wired article isn’t very long and is well worth your time to read. But I’ll assume you’re not as fascinated by this kind of thing as I am and summarize it as follows.

Essentially it’s not a new discovery — apart from its novel application to the internet — but concerns probability theory statistics and is a “long-known feature of statistical distributions” known as “Zipf, Power laws, Pareto distributions and/or general Lévy distributions.”

Wikipedia explains it thusly:

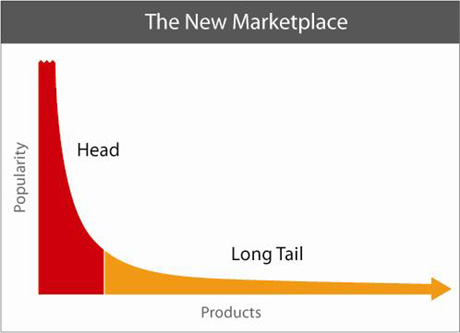

In these distributions a high-frequency or high-amplitude population is followed by a low-frequency or low-amplitude population which gradually “tails off”. In many cases the infrequent or low-amplitude events—the long tail, represented here by the yellow portion of the graph—can cumulatively outnumber or outweigh the initial portion of the graph, such that in aggregate they comprise the majority.

Such distributions are surprisingly common. In standard English, the word “the” is the most common word and other short words such as “of”, “is” and “have” are also quite common. These common words are vastly more common than most other words. For example, about 12% of all words are “the” (while “barracks” occurs less than 1 out of 50,000 words), but cumulatively, words roughly as rare as “barracks” make up about a third of all text. These rare words are the long tail in English vocabulary.

Wikipedia also has a nice further description of it including its origins and many examples. And Anderson’s blog contains a nutshell version of the theory.

A short digression is in order here. I take a decidedly odd pleasure in reading about economics, the dismal science. Over the last several years I’ve digested several overviews of the history of economics, its leading lights, and so on. I’m not proud of it mind you, I think of it more as a guilty pleasure. Stuff like Thomas Frank’s One Market Under God, Robert Heilbroner’s The Worldly Philosophers and even Freakonomics, which was actually quite interesting. I especially enjoy the writings of Paul Krugman, the Princeton professor who writes a column for the New York Times. His collection of columns, The Great Unraveling, is a terrific — if occasionally depressing — read. And you thought I did nothing but drink beer.

So after reading Anderson’s article, I was struck by how many parallels there were to the beer industry even though his focus was business on the internet and how it is unmaking traditional business models. This analogy seems especially true concerning the relationship between mainstream or big breweries and craft beer. It doesn’t suggest how a new model of distribution might work the way it does on the internet, but it goes a long way toward explaining many of the problems craft brewers are having getting their products to market and in developing greater demand for them. If you’re still with me so far, what follows is my feeble attempt to examine those similarities. I think there are some valuable lessons that may be drawn from such a comparison of economic models.

An Analysis of Chris Anderson’s “Long Tail” Theory as Applied to the Beer Industry

Here is Anderson, in the original article, explaining the underlying reasons that an old book that was almost out-of-print became a bestseller thanks to Amazon.com, word of mouth and their snowballing effects.

It is an example of an entirely new economic model for the media and entertainment industries, one that is just beginning to show its power. Unlimited selection is revealing truths about what consumers want and how they want to get it in service after service, from DVDs at Netflix to music videos on Yahoo! Launch to songs in the iTunes Music Store and Rhapsody. People are going deep into the catalog, down the long, long list of available titles, far past what’s available at Blockbuster Video, Tower Records, and Barnes & Noble. And the more they find, the more they like. As they wander further from the beaten path, they discover their taste is not as mainstream as they thought (or as they had been led to believe by marketing, a lack of alternatives, and a hit-driven culture).

This is exactly how and why (at least in part, there other factors to be sure) mainstream beer outsells craft beer by such a wide margin. Think of mainstream beer as the bland stuff churned out by the world’s biggest breweries and made to appeal to the lowest common denominator. To be fair these breweries for the most part do make products that are well-made and very consistent. But even these breweries are beginning to acknowledge that they are virtually indistinguishable from one another. What’s the one thing they all have in common? Availability. They’re available literally everywhere beer is sold, even at the most hardcore of craft beer taphouses (with just a couple of notable exceptions). Everybody carries the hits with very few “deep catalog” beers. (Remember we’re talking hypothetically here.) We really can never know what consumers will buy if they’re continually offered only an extremely narrow selection of all available beers. If, however, every beer that is packaged in the world were offered in every store and given equal weight (same placement, same quantities, etc.), what would the sales breakdowns look like then? I would bet dollars to donuts that many, many people would choose a different beer than their usual choice, even after the initial novelty of such selection wore off. As Anderson notes, people would be more apt to experiment and they’d “discover their taste is not as mainstream as they thought (or as they had been led to believe by marketing, a lack of alternatives, and a hit-driven culture.” Every convert I’ve ever helped along reaches a point where they realize they’d been sold a bill of goods about what beer is supposed to taste like. And once they discover how diversely rich and flavorful good beer is, very few will willingly make the trip back to the mainstream.

Most people are lazy about some decisions in their lives — I count myself among them — and take the easiest path available. You have to. None of us can be passionate about everything. Choices must be made. For example, to me all laundry detergents are the same. I could care less which one I buy and usually end up buying the cheapest one. Now I suppose there are some people who are quite passionate about their laundry detergent. My grandmother never used anything but Tide. She refused to use any other detergent. So convinced was she that Tide was the superior one that she would turn down even free alternatives. My point is some choices we have to make are done on a kind of autopilot. This human tendency makes availability perhaps the single most important reason for current buying patterns in all manner of things, including beer. They’re all the same, right? Does that sound overly simplistic? Not when you consider that craft beer has only a 3.5% market share, meaning 96.5% percent believe essentially just that.

Anderson continues:

For too long we’ve been suffering the tyranny of lowest-common-denominator fare, subjected to brain-dead summer blockbusters and manufactured pop. Why? Economics. Many of our assumptions about popular taste are actually artifacts of poor supply-and-demand matching — a market response to inefficient distribution.

Mainstream beers certainly fit the lowest-common-denominator epithet. Very few people can actually taste the difference between American-style lagers which, although based upon pilsners, bear as much resemblance to their progenitors as frogs do to man, despite a common ancestry. Without trying to sound condescending, many people think these taste good because they’ve been told they taste good … over and over again.

But most of us want more than just hits. Everyone’s taste departs from the mainstream somewhere, and the more we explore alternatives, the more we’re drawn to them. Unfortunately, in recent decades such alternatives have been pushed to the fringes by pumped-up marketing vehicles built to order by industries that desperately need them.

Hit-driven economics is a creation of an age without enough room to carry everything for everybody.

Historically, all breweries were essentially local or regional at most. There were no national breweries until after the invention of refrigeration. Beer did not travel well enough before that time and so breweries were limited in the territory in which they could sell their beers. Several factors changed in a short space of time, making national breweries feasible for the first time after World War 2. Keeping beer cold, of course, came before that time but a national media and especially television that made reaching the entire nation possible was also very important. It’s no coincidence that tomorrow is the 55th anniversary of Pabst becoming the first brewer to advertise in color when CBS broadcast a special one-hour inaugural show (June 25, 1951). It was there very ability to do so that allowed Pabst to become nationally recognized.

Then there was post-war prosperity and the national highway system, which made shipping to anywhere in the U.S. more economical. These caused products of all stripes from soup to nuts to create national identities. In order to appeal to this much wider consumer base, they were generally re-tooled to appeal to the lowest-common denominator. For beer, this actually began during the war, when the military requested beer for the troops that was watered down so as to avoid soldiers too inebriated to fight. Many returned with a taste for the bland.

So the bland American-style lagers developed over time to appeal to almost everyone or at least offend no one. Add to that immense advertising and marketing budgets with television and sports sponsorships and you can create national brands. Fortunes were won and lost as the breweries battled one another for dominance on a national scale. Brewing history is littered with the losers of this period. Hundreds of once prominent and popular regional breweries are gone. Our brewing heritage itself all but stamped out in the name of commerce. Prior to the late 1970s, the American beer scene was on the brink of extinction. Our most popular beers made us the laughingstock of the world. There were a few pockets of resistance here and there, but by and large the war was almost over. But then a backlash began that became the microbrewery revolution, which in twenty-five or so years has created a beer culture that is the envy of the world. More different styles of beer are now brewed in America than any other place in the world. Almost all innovation in brewing is happening at the craft beer level. American beers consistently win a higher proportion of awards in international competitions. By any measure, this is a phenomenal achievement. It’s too bad 96.5% of Americans are scarcely aware of it.

The only companies that can afford a seat at the national advertising table are the mainstream breweries. Therefore their voices are the only ones that can be heard. This unrelenting barrage of marketing has created a market so propped up that it would likely collapse if they suddenly stopped. This perpetual marketing machine can be compared to running on a treadmill. As long as you’re moving your legs you’ll stay in the same place but stop and you’ll be thrown off.

Anderson explains some reasons for this phenomenon:

[T]he [entertainment] industry has a poor sense of what people want. Indeed, we have a poor sense of what we want. We assume, for instance, that there is little demand for the stuff that isn’t carried by Wal-Mart and other major retailers; if people wanted it, surely it would be sold. The rest, the bottom 80 percent, must be subcommercial at best.

But as egalitarian as Wal-Mart may seem, it is actually extraordinarily elitist. Wal-Mart must sell at least 100,000 copies of a CD to cover its retail overhead and make a sufficient profit; less than 1 percent of CDs do that kind of volume. What about the 60,000 people who would like to buy the latest Fountains of Wayne or Crystal Method album, or any other nonmainstream fare? They have to go somewhere else. Bookstores, the megaplex, radio, and network TV can be equally demanding. We equate mass market with quality and demand, when in fact it often just represents familiarity, savvy advertising, and broad if somewhat shallow appeal. What do we really want? We’re only just discovering, but it clearly starts with more.

This goes back to shoppers walking down the beer aisle week after week, month after month, year after year and seeing the same beers every time. If there were a demand for other beers, the stores would stock them, right? How do they know if there’s a demand for something they don’t carry. How many people ask about products they don’t see? In my experience, unless it’s peculiarly popular for some reason, hardly ever. Think about your own experience. Your local grocery store doesn’t carry the jam you like. But they do have a dozen other brands that look fine. Are you more likely to just choose from the available choices or inquire (or complain) and give up jam on your morning toast? If you’re like most if us, you’ll buy the Smuckers without a second thought and get on with your life.

Also, as the mainstream domestic brewers are experiencing a loss of revenue lately craft beer is showing rising consistent growth. This has led many industry observers to conclude that consumers are demanding a greater diversity of available flavors. This would seem an ideal opportunity for craft brewers — and especially the regional players — to step in and give the people what they’re clamoring for. But the mainstream brewers will not allow that to happen if they can possibly help it. And for the most part they do have the resources, necessary clout and wherewithal to do just that. This explains why many big breweries are frantically adding to their portfolios by creating new products, buying existing ones and pairing with successful import and domestic breweries in distribution deals. Because availability is control. The more products they can control, the more market share they can control and the more they can squeeze competition out of the marketplace while providing to the market a illusory perception of greater diversity while actually doing the opposite.

To get a sense of our true taste, unfiltered by the economics of scarcity, look at Rhapsody, a subscription-based streaming music service (owned by RealNetworks) that currently offers more than 735,000 tracks.

Chart Rhapsody’s monthly statistics and you get a “power law” demand curve that looks much like any record store’s, with huge appeal for the top tracks, tailing off quickly for less popular ones. But a really interesting thing happens once you dig below the top 40,000 tracks, which is about the amount of the fluid inventory (the albums carried that will eventually be sold) of the average real-world record store. Here, the Wal-Marts of the world go to zero – either they don’t carry any more CDs, or the few potential local takers for such fringy fare never find it or never even enter the store.

The Rhapsody demand, however, keeps going. Not only is every one of Rhapsody’s top 100,000 tracks streamed at least once each month, the same is true for its top 200,000, top 300,000, and top 400,000. As fast as Rhapsody adds tracks to its library, those songs find an audience, even if it’s just a few people a month, somewhere in the country.

This is the Long Tail.

In the world of beer, the long tail is currently evident only in large liquor chains such as Beverages & more and their ilk along with the few beer-only stores like San Francisco’s new City Beer Store, Belmont Station and Bottleworks. The main problem is that beer cannot be effectively dispensed digitally, meaning you can’t download a beer. Pity. How great would it be to have a USB tap from which you could download any beer you wanted. But enough fantasy. Because of this dilemma, the long tail does not currently present a solution to this predicament. But it does provide some useful reasons why things are the way they are. Perhaps that knowledge will eventually suggest a way.

Anderson concludes:

What’s really amazing about the Long Tail is the sheer size of it. Combine enough nonhits on the Long Tail and you’ve got a market bigger than the hits. Take books: The average Barnes & Noble carries 130,000 titles. Yet more than half of Amazon’s book sales come from outside its top 130,000 titles. Consider the implication: If the Amazon statistics are any guide, the market for books that are not even sold in the average bookstore is larger than the market for those that are. In other words, the potential book market may be twice as big as it appears to be, if only we can get over the economics of scarcity.

So the real goal of craft brewers appears to be overcoming the “economics of scarcity.” This may mean creating new models of distribution. Maybe it’s time to revisit self-distribution again or consider pooling resources to create craft specialty distributors. Many such attempts have failed in the past but maybe the business world would be more accepting of them in today’s climate. Certainly Stone Brewing seems to be making this idea work. Businesses are generally in favor of products that sell and make them money.

Many beer distributors have pushed a narrow range of products on retailers because they themselves were manipulated and bullied to do so. For example, I have heard accounts of Augie Busch sitting in a distributor’s conference room petulantly throwing bottles of craft beer so they exploded with a jangling crash against the wall to show his disdain for any product not under his thumb because the businessman running the beer distributor had the temerity — and as it turns out foresight — to sell products his customers actually wanted. But now the mainstream beer slump is hurting them, too, which is what is driving the big guys to scramble to fix this slump. Otherwise, their distributors will look more favorably on carrying products that are selling.

Opportunity is knocking on the door. We should answer it. At the very least we should capitalize on it. There are probably other ways to address this problem that we haven’t even thought of yet. But in an industry that so thrives on innovation, we should be able to come up with something. Time to think outside the cold box.

This is the longneck tail.

Anheuser-Busch’s New “Long Tail Division“

Business Innovation Insider is a blog in conjunction with FORTUNE’s Innovation Forum (a conference held annually in late November), reports on business innovation. A piece in yesterday’s edition was entitled “The long tail of the alcohol distribution curve” and concerned a new division created by Anheuser-Busch called “Long Tail Libations.” The goal of this new division is to develop “more “niche” alcohol products to supplement the company’s “hits”. From this it seems a reasonable inference that the division was set up to explore niche markets down along the long tail of the market.

The Wall Street Journal, explained Anheuser-Busch’s expansion into new markets:

Anheuser-Busch, battling industry market-share losses to purveyors of wine and liquor, is hinting that it will make an effort to enter the liquor industry… Anheuser has made some tentative moves into the liquor business. Last year, it formed a separate division, Long Tail Libations, to develop, test and market distilled spirits. Its first product, Jekyll & Hyde, a liqueur, is being test marketed in a handful of places. Over the past few years, the St. Louis-based brewer also has joined forces with Bacardi to produce flavored malt beverages, so-called malternatives, under the Bacardi Silver label.

There’s been a lot of attention paid to remarks made by Augie 4.0 at a state regulator’s meeting where he stated that they “might” consider going into the spirits business. Also, on February 9 of this year, A-B filed a trademark application for a distilled spirit called Faust, a name they’ve used in the past for their “American Originals” series of beers, which was part of their original assault on craft beer.

But as Jim Arndorfer, editor of Miller’s BrewBlog, wryly pointed out, given that they’ve created this new division— Long Tail Libations — and are test marketing a liqueur, “doesn’t that mean they’re already ‘in the business'”? All of these stories seem to be focusing on the supposed “possibility” of A-B spirits while ignoring the fact that they are already making them. The Business Journal of Jacksonville article — which is the one most media ran — used a headline that said A-B “hints at liquor market entrance.” It seems to me if you have an actual spirit people can hold in their hands and buy then you’ve moved well beyond just “hinting.”

But of course, that’s not their only tactic. They developed dozens of new beers and beer-like malt beverages and are testing many of them in the marketplace. I tried a number of them at last year’s Great American Beer Festival. They’ve introduced two new stealth micros into the organic market. Distribution deals and/or bought into regional brewers such as Goose Island with many more rumored to be in negotiations to be added to their craft alliance that currently includes Redhook and Widmer Brothers. They’ve signed distribution agreements with several imported beers in the last few months (Tiger and Grolsch) and bought outright the Chinese Harbin. And, of course, they recently bought the domestic brand Rolling Rock. Reportedly talks are ongoing with InBev to distribute their European products. They’re even currently trying to create a gluten-free beer.

From the Business Innovation Insider:

As the president of Anheuser-Busch’s U.S. beer operations pointed out, “We will have to re-evaluate our business model going forward in terms of expanding beyond beer and broadening our position within the total alcohol industry.” Does that sound like a Long Tail strategy or what? As the Liquor Snob points out, the new Jekyll & Hyde drink is about the furthest thing from good ol’ Budweiser beer:

“The company is currently dipping its toe in the hard liquor pond, testing out a new liquor it’s developed called Jekyll and Hyde, which comes as two liquors designed to be mixed together. The product comprises of two liqueur bottles. Jekyll is a scarlet red, sweet spirit tasting of wild berries, while Hyde is an herbal tasting, black spirit that floats on top when poured over the red-colored Jekyll. The two products are meant to be served together, although consumers can drink them separately as well, the company said.

Can a box wine be far behind? A partnership with Gallo? They’re obviously leaving no stone unturned so why not?

The important thing to be learned from all this is that Anheuser-Busch knows about Chris Anderson’s Long Tail theory and is moving toward putting it into practice in a way he probably didn’t envision. That they have the business acumen and resources to pull it off — failing any active resistance — seems to me all but a fait accompli.

This revelation that A-B has embraced the long tail theory also makes their recent behavior more understandable and explainable. For example, when Wild Hop Lager first appeared, many asked why such a large company would go after the organic market, which is such a small market. But as long tail theory expounds, it’s not about the size of each market. It’s all the small markets combined that add up to something. And A-B is trying to move into as many niche markets as possible. From organic beers to small imported beers like Tiger and Grolsch to national brands like Rolling Rock. They’re trying to own both the head and the tail — in other words dominate every facet of the beer (and alcohol) business. They won’t be satisfied by anything less than a total sweeping victory.

When craft beers first came into wider public consciousness in the mid-1990s, the big breweries did respond with their own faux craft beers. Coors had Blue Moon and Killian’s. Miller had Red Plank Brewery with its popular Icehouse along with the many regional brands they’d bought up and shut down during the heady days of the 1980s. Anheuser-Busch had their American Original Series, Elk Mountain, Michelob, Red Wolf, Tequiza and Pacific Ridge Pale Ale.

The second wave of attacks from A-B have included Anheuser World Select, Antarctica Rio Cristal, Aruba Red, BE (B-to-the-E), Bare Knuckles Stout, Beach Bum Blonde Ale, Blue Horizon (a Blueberry Lager), Brewhouse Lager, Brew Masters Private Reserve, Budweiser Select, Busch Hefeweizen, Demon’s Hop Yard IPA, Devil Ray Red, Devon’s Original Shandy, Foxhound Lager, Jack’s Pumpkin Spice Ale, Killarney’s Red Lager, Leaf Peeper Pils, Lone Palm Ale, Michelob Ultra, 9th Street Market, Phillies Red Lager, Red, Safari Amber, Spring Heat Spiced Wheat, Stone Face Ale, Stone Mill Pale Ale, Tilt, Tomahawk Amber Ale, Wild Blue, Wild Hop Lager, Winter Bourbon Cask Ale, and ZiegenBock. Whew, that’s a long list, though it’s not even an exhaustive one. There are likely many more that were only test marketed that few are aware of anymore. And there are undoubtedly new product tests going on and/or planned right now. If you throw enough up against the wall, some of them are bound to stick.

To understand why this is so troubling, you have to get inside the mind of retailers. Big retailers employ buyers, usually many buyers, whose job it is to decide which products will be carried and in what quantities, placement, which are advertised, and on and on. Most are, of course, overworked and underpaid. I was one of them once upon a time. The more products you can buy from the fewest sources the better. It makes you more efficient if you don’t have to meet with what seems like an endless stream of suppliers. That’s one of the reasons beer distributors have been so successful. A buyer can meet with one person who represents many, many brands. Only the bigger players get an audience with buyers of big chains. The rest have to work through distributors, sales rep. companies, etc. So if your local Anheuser-Busch distributor (several of which, where legal, are actually owned by A-B) carries not only your big sellers (Bud, Bud Light) but also products that cover a wide range of niches you’d like to fill then it will be very tempting to buy most everything in their portfolio. Add to that the leverage of being the biggest seller and you can see why most succumb to that temptation so willingly. It just makes good business sense, most will tell you. The unwritten and unspoken agreement is that those who support the best sellers by carrying all their products will get the most favorable terms and make the most money. If you know the brands, you can see this play out in almost every convenience store, gas station, drug store and grocery store that carries beer. You can actually walk down the aisle and see that all the beer there comes from a very small number of suppliers/distributors. The diversity you see is mostly illusory.

This makes it very, very difficult for small brewers to get their beer into larger chain stores at all. It’s the reason A-B’s Craft Alliance with Redhook and Widmer (with more new ones coming) has been so successful. It’s why in stores with few beer skus, if you see any craft beer at all, you’ll almost always see Redhook or Widmer. For some reason this has damaged Redhook’s reputation (many derisively now call them “Budhook“) but left Widmer relatively unscathed. But Widmer has been the more successful of the two, which has allowed them to maintain their independence and, perhaps more importantly, has allowed them to maintain the perception of Independence, which has kept consumer confidence high. Plus Rob and Kurt are great people who support the craft beer industry. But the real danger is that having so many brands under the control of one company makes it increasingly easy to squeeze out everybody else. Bud distributors are under increasing pressure to carry only A-B brands so the strategy is to give the distributors what they want within A-B so they don’t have any reason to look elsewhere for products their customers (the retailers) want. This may make the grocery chain happy, but it’s a disaster for almost everybody else. And it’s getting worse and worse. There’s much less diversity on the average grocer’s beer shelf than there was ten years ago.

All of this taken together reveals a strategy in which the goal is to literally cover every imaginable market with an eye toward either destruction or domination. Either will suit shareholder aims. It’s been the method of big corporations since time immemorial, though A-B has raised it to something of a perverse fine art. I don’t think I’ve ever seen it on this scale. The sheer number of brands hints at the soberness of the endeavor. You know they’re not fooling around. We must take this threat seriously, too. I think we have to acknowledge that it is a direct assault. To not do so is to be unable to craft the proper response. And while everything is going for the craft beer industry these days with excellent growth, renewed interest and even occasional good press, we are still quite vulnerable and our position remains precarious. So we must, I think, proceed with extreme caution. And we must act as a cohesive group, which is why I am so worried about the Goose Island alliances in the industry. The possible ramifications for that development could be dire indeed. The beachhead we’ve established along the long tail must be defended. Our very survival depends on it.